[ad_1]

There’s an old trope in business and technology: “there are only two ways to make money in business: one is to bundle; the other is unbundle.” This is true in traditional industries but even more true in the world of crypto and DeFi, given its permissionless nature. In this piece, we’ll look at the surging popularity of modular lending (and those enlightened folks that are already post-modular), and examine how it’s upending the DeFi lending stalwarts. With unbundling, a new market structure emerges with new value flows – who will benefit most?

– Chris

There’s already been a great unbundling at the core base layer, where Ethereum used to have a single solution for execution, settlement and data availability. However, it has since moved toward a more modular approach, with specialized solutions for each core element of the blockchain.

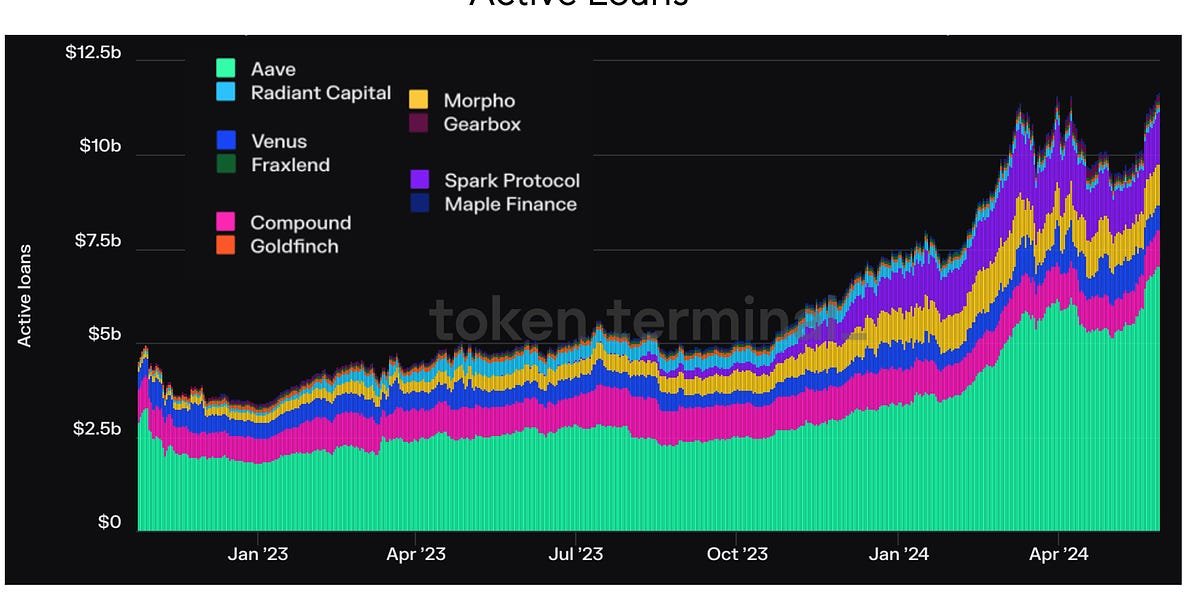

This same pattern is playing out in the DeFi lending space. The first successful products were those with everything self-contained. While the original three DeFi lenders – MakerDAO, Aave, and Compound – had many moving parts, they all operated in a pre-defined structure set by their respective core teams. These days, however, growth in DeFi lending has come from a new crop of projects that split up the core functions of a lending protocol.

These projects are creating isolated markets, minimizing governance, separating risk management, liberalizing oracle responsibilities, and removing other single dependencies. Others are creating easy-to-use bundled products that put multiple DeFi legos together to offer a more all-encompassing lending product.

This new push to unbundle DeFi borrowing has been memed into Modular Lending. We are big fans of memes here at Dose of DeFi, but have also seen new projects (and their investors) try to hype new narratives on the market more for their bags than because there’s some underlying innovation (looking at you, DeFi 2.0).

Our take: the hype is real. DeFi lending will go through a similar metamorphosis as the core base layer – where new modular protocols emerged like Celestia while existing incumbents shifted their roadmaps to become more modular – as Ethereum has done as it continues to unbundle itself.

In the immediate term, the key competitors are forging different paths. Morpho, Euler, Ajna, Credit Guild and others are seeing success as new modular lending projects, while MakerDAO moves toward a less concentrated SubDAO model. Then you have the recently announced Aave v4, which is moving in the modular direction, mirroring Ethereum’s architecture shift. These paths being carved-out now could well determine where the value accrues in the DeFi lending stack over the long term.

There are generally two approaches to building complex systems. One strategy is to focus on the end-user experience and ensure the complexity doesn’t hinder usability. This means controlling the entire stack (as Apple does with its hardware and software integration).

The other strategy focuses on enabling multiple parties to build individual components of a system. Here, the centralized designers of the complex system focus on core standards that create interoperability, while relying on the market to do the innovation. This is seen with the core internet protocols, which haven’t changed, while the applications and businesses that have built on top of TCP/IP have driven innovation on the internet.

This analogy could also be applied to economies, where a government is seen as the base layer, a la TCP/IP, ensuring interoperability through the rule of law and social cohesion, where economic development then occurs in the private sector built on top of the governance layer. Neither of these approaches work all the time; many companies, protocols, and economies operate somewhere on the spectrum.

Those that support the modular lending thesis believe that innovation in DeFi will be driven by specialization in each part of the lending stack, rather than focusing on just the end-user experience.

A key reason for this is the desire to eliminate single dependencies. Lending protocols require close risk monitoring and a small issue can lead to catastrophic loss, so building redundancy is key. Monolithic lending protocols have introduced multiple oracles in case one fails, but modular lending takes this hedging approach and applies it to every layer of the lending stack.

For every DeFi loan, we can identify five key components that are needed – but can be modified:

-

A loan asset

-

A collateral asset

-

Oracle

-

Max loan-to-value (LTV)

-

Interest rate model.

These components must be closely monitored to ensure a platform’s solvency and prevent bad debt accruing because of rapid price changes (we could also add the liquidation system to the five components above).

For Aave, Maker, and Compound, token governance makes decisions for all assets and users. Initially, all assets were pooled together and shared the risk of the whole system. But even the monolithic lending protocols have moved quickly into creating isolated markets for each asset, to compartmentalize the risk.

Isolating markets is not the only thing you can do to make your lending protocol more modular. The real innovation is happening in new protocols that are reimagining what’s necessary in a lending stack.

The biggest players in the modular world are Morpho, Euler and Gearbox:

-

Morpho is the clear leader of modular lending at the moment, although it seems recently uncomfortable with the meme, trying to morph into “not modular, not monolithic, but aggregated”. With $1.8 billion in TVL, it’s arguably already in the top tier of the DeFi lending industry as a whole, but its ambitions are to be the largest. Morpho Blue is its primary lending stack, on which it’s permissionless to create a vault tuned to whatever parameters it desires. Governance only enables what can be modified – currently five different components – not what those components should be. That is configured by the vault owner, typically a DeFi risk manager. The other major layer of Morpho is MetaMorpho, an attempt to be the aggregated liquidity layer for passive lenders. This is a particular piece focused on end-user experience. It’s akin to Uniswap having the DEX on Ethereum and also Uniswap X for efficient trade routing.

-

Euler launched its v1 in 2022 and generated over $200 million in open interest before a hack drained nearly all protocol funds (although they were later returned). Now, it’s preparing to launch its v2 and reenter a maturing modular lending ecosystem as a major player. Euler v2 has two key components. One, the Euler Vault Kit (EVK), which is a framework for creation of ERC4626 compatible vaults with additional borrowing functionality, enabling them to serve as passive lending pools, and two, the Ethereum Vault Connector (EVC), which is an EVM primitive that primarily enables multi-vault collateralisation, i.e., multiple vaults can use collateral made available by one vault. V2 has a planned Q2/Q3 launch.

-

Gearbox provides an opinionated framework that is more user centric, i.e. users can easily set up their positions without too much oversight, regardless of their skill/knowledge level. Its primary innovation is a “credit account” which serves as an inventory of allowable actions and whitelisted assets, denominated in a borrowed asset. It’s basically an isolated lending pool, analogous to Euler’s vaults, except that Gearbox’s credit accounts hold both user collateral and borrowed funds in one place. Like MetaMorpho, Gearbox demonstrates that a modular world can have a layer that specializes in packaging for the end user.

Specialization in parts of the lending stack presents an opportunity to build alternative systems that may target a specific niche or bet on a future growth driver. Some leading movers with this approach are listed here:

-

Credit Guild intends to approach the already-established pooled lending market with a trust-minimized governance model. Existing incumbents, such as Aave, have very restrictive governance parameters, and more often than not this results in apathy among smaller token holders since their votes seemingly don’t change much. Thus, an honest minority in control of most tokens is responsible for most changes. Credit Guild turns this dynamic on its head by introducing an optimistic, vetocracy-based governance framework, which stipulates various quorum thresholds and latencies for varying parameter changes, while integrating a risk-on approach to deal with unforeseen fallouts.

-

Starport’s ambitions are a bet on the cross-chain thesis. It has implemented a very basic framework for composing different types of EVM-compatible lending protocols. It’s designed to handle data availability and term enforcement for the protocols built atop it via two core components:

1. The Starport contract, which is responsible for loan originating (term definition) and refinancing (term renewal). It stores this data for the protocols built atop the Starport kernel and makes it available when needed.

2. The custodian contract, which primarily holds the collateral of borrowers on originating protocols atop Starport, and ensures that debt settlements and closure proceed according to the terms defined by the originating protocols and stored in the Starport contract.

-

Ajna boasts a truly permissionless model of oracleless pooled lending with no governance at any level. Pools are set up in unique pairs of quote/collateral assets provided by lenders/borrowers, allowing users to assess demand for either of the assets and allocate their capital accordingly. Ajna’s oracle-less design is borne off lenders’ ability to specify the price at which they’re willing to lend, by specifying the amount of collateral a borrower should pledge per quote token they hold (or vice versa). It will be especially appealing to the long tail of assets (much like Uniswap v2 does for small-ish tokens).

The lending space has attracted a slew of new entrants, which has also reinvigorated the largest DeFi protocols to launch new lending products:

-

Aave v4, which was announced last month, is awfully similar to Euler v2. It comes after Aave zealot Marc “Chainsaw” Zeller said that Aave v3 would be the end state of Aave because of its modularity. Its soft liquidation mechanism was pioneered by Llammalend (explainer below); its unified liquidity layer is also similar to Euler v2’s EVC. While most of the impending upgrades aren’t novel, they’re also yet to be widely tested in a highly liquid protocol (which Aave already is). It’s crazy how successful Aave has been at winning market share on EVERY chain. Its moat may be shallow, but it’s wide, and gives Aave a extremely strong tailwind.

-

Curve, or more informally Llammalend, is a series of isolated and one-way (non-borrowable collateral) lending markets in which crvUSD (already minted), Curve’s native stablecoin, is used as either the collateral or debt asset. This enables it to combine Curve’s expertise in AMM design and offer unique opportunities as a lending market. Curve has always driven on the left side of the road in DeFi, but it’s worked out for them. It has as such carved out a significant niche in the DEX market, aside from the Uniswap goliath, and is making everyone question their tokenomics skepticism with the success of the veCRV model. Llamalend appears to be another chapter in the Curve story:

-

Its most interesting feature is its risk management and liquidation logic, which is based on Curve’s LLAMMA system that enables ‘soft liquidations’.

-

LLAMMA is implemented as a market making contract that encourages arbitrage between an isolated lending market’s assets and external markets.

-

Just like a concentrated liquidity Automated Market Maker (clAMM eg. Uniswap v3), LLAMMA evenly deposits a borrower’s collateral across a range of user-specified prices, referred to as bands, where the offered prices are greatly skewed in relation to the oracle price in order to ensure arbitrage is always incentivised.

-

In this way, the system can automatically sell (soft-liquidate) portions of the collateral asset into crvUSD as the former’s price decreases past bands. This decreases the overall loan health, but is decidedly better than outright liquidations, especially considering the explicit support of long-tail assets.

-

Whew. Curve founder Michael Egorov making over-engineered criticisms obsolete since 2019.

Both Curve and Aave are hyper focused on the growth of their respective stablecoins. This is a good long-term strategy for fee-extraction (ahem, revenue) capability. Both are following in the footsteps of MakerDAO, which has not given up on DeFi lending, spinning off Spark as an isolated brand that has had a very successful past year even without any native token incentives (yet). But a stablecoin and the crazy ability to print money (credit is a hell of a drug) are just gigantic opportunities long term. Unlike lending, however, stablecoins do require some onchain governance or offchain centralized entities. For Curve and Aave, which have some of the oldest and most active token governance (behind MakerDAO of course), this route makes sense.

The question we can’t answer is what is Compound doing? It was once DeFi royalty, kickstarting DeFi summer and literally establishing the yield farming meme. Obviously, regulatory concerns have constricted its core team and investors from being more active, which is why its market share has dwindled. Still, much like Aave’s wide, shallow moat, Compound still has $1 billion in open loans and a wide governance distribution. Just recently, some have picked up the baton to develop Compound outside the Compound Labs Team. It’s unclear to us what markets it should focus on – perhaps large, blue-chip markets, especially if it can gain some regulatory advantage.

The DeFi lending original three (Maker, Aave, Compound) are all rejiggering their strategies in response to the shift to a modular lending architecture. Lending against crypto collateral was once a good business, but when your collateral is onchain, your margins will compress as markets become more efficient.

This doesn’t mean there are no opportunities in an efficient market structure, just that no one can monopolize their position and extract rent.

The new modular market structure enables more permissionless value capture for proprietary bodies such as risk managers and venture capitalists. This enables a more skin-in-the-game approach to risk management, and directly translates to better opportunities for end users, since economic losses will cause much harm to a vault manager’s reputation.

A great example of this is the recent Gauntlet-Morpho drama during the ezETH depeg.

Gauntlet, an established risk manager, ran an ezETH vault which suffered losses during the depeg. However, since the risk was more defined and isolated, users across other metamorpho vaults were mostly insulated from the fallout, while Gauntlet had to provide post-mortem evaluations and take responsibility.

The reason Gauntlet launched the vault in the first place was because it felt its future prospects were more promising on Morpho, where it could charge a direct fee, versus providing risk management advisory services to Aave governance (which tends to focus more on politiking than risk analysis – you try wining and dining a chainsaw).

Just this week, Morpho founder, Paul Frambot, revealed that a smaller risk manager, Re7Capital, which also has a great research newsletter, was earning $500,000 in annualized onchain revenue as a manager of Morpho vaults. While not huge, this demonstrates how you can build financial companies (and not just degen yield farming) on top of DeFi. It does raise some long-term regulatory questions, but that’s par for the course in crypto these days. And moreover, this won’t stop risk managers from topping the ‘who’s set to gain the most’ list for the future of modular lending.

-

U.S. House Approves Crypto FIT21 Bill With Wave of Democratic Support Link

-

Block Analitica proposes new interest rate framework for MakerDAO Link

-

DOJ charges two brothers with fraud for baiting MEV bots Link

-

Maker founder Rune proposes ‘PureDai’ made up of only crypto collateral Link

-

EIP-7706 would add a new gas type specific for calldata Link

-

ENS aims to launch own L2, likely with zkSync Link

-

Token flow regulatory chart in light of recent US progress Link

That’s it! Feedback appreciated. Just hit reply. Thanks to Zhev for major help on breaking down the major modular players. So much green in Tennessee in the spring.

Dose of DeFi is written by Chris Powers, with help from Denis Suslov and Financial Content Lab. I spend most of my time contributing to Powerhouse, an ecosystem actor for MakerDAO. Some of my compensation comes from MKR, so I’m financially incentivized for its success. All content is for informational purposes and is not intended as investment advice.

[ad_2]

Source link